Technological Innovations in Cross-Border Payment Systems in 2026: By Satyam Chaturvedi

The number of cross-border transactions has risen significantly in the last few years.

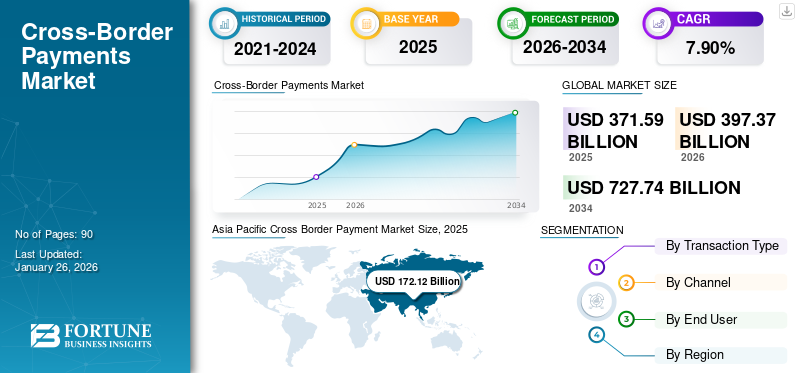

According to Fortune Business Insights, the global cross-border payment market size was valued at USD 371.59 billion in 2025 and is expected to grow from USD 397.37 billion in 2026 to USD 727.74 billion by 2034, exhibiting a CAGR of 7.90%.

While it generally seemed a headache to carry out an international transaction, today, technological advancements have completely transformed the scenario, making these transactions almost instantaneous.

One can never deny the fact that technological innovations have played a crucial role in creating, executing, and transforming the entire cross-border payments system.

In 2026, the true definition of globalization and global outreach has certainly changed for businesses as they are now more eager to work globally.

With cross-border transactions becoming more and more accessible and manageable by financial institutions, the global marketplace has seen massive growth, thanks to several technological advancements.

Wondering what technological innovations have led to this global cross-border payment revolution? Well, that is exactly what this post is about. Without further ado, let’s look at 4 technologies that are set to change the way cross-border payment systems work.

Technologies Used in Cross-Border Payments & Their Impact

While solutions like mobile payments, instant payment apps, peer-to-peer transfer apps, etc. have made cross-border payments accessible to the user, there are several modern payment technologies and trends that bring security and efficiency to these transactions.

Some of the core technological innovations that are set to make a difference in the cross-border payment scenario are as follows –

-

Blockchain and distributed ledger technology (DLT)

One of the most crucial issues that businesses face during cross-border payments is the delayed account settlement.

Use of Blockchain and Distributed Ledger Technology (DLT) allows settlement in minutes as it is autonomous and is not affected by external factors such as bank closures or holidays. This instant settlement resolves a lot of issues and encourages more and more businesses to go global, as hindrance in cash-flow and rotation is no longer a point of concern, even for small businesses.

Blockchain brings transparency and security to cross-border payments through its decentralized ledger, which is immutable. This allows the transaction to be super accurate, safe, and irreversible.

-

Smart contracts for payments

Another issue that troubles global businesses that depend on cross-border payments is the higher cost of execution.

With heavy charges and multiple parties involved in traditional cross-border payments, it was nothing less than painful for a business to accept cross-border payments, often resulting in lost business. However, with the use of smart contracts for payments, the process becomes super efficient as all the middlemen and third parties are replaced by automated smart contracts.

The use doesn’t end here, as smart contracts also help in automated compliance checks and the flow of payments for streamlined workflows. Smart contracts work heavily with the Blockchain DLT supply chain.

-

AI/ML for fraud detection and AML compliance

Generally, when we talk about Anti-Money Laundering compliance, it is always considered as a reactive measure towards money laundering practices for a platform.

Thanks to the integration of artificial intelligence and machine learning in cross-border payment systems, it has become more of a proactive solution. The use of AI helps in yielding behavioural analytics, which can be used in further anomaly detection in transaction processing, allowing the system to catch fraudulent transactions and activities.

Machine learning, on the other hand, can help in capturing the essence of how cross-border transactions are generally carried out from one business to another. This way, when the transaction volume or amount is significantly varied, a compliance check and precautionary measures are triggered.

-

APIs for integration with legacy banking systems

What makes it all possible for legacy banks is the use of APIs. In case you are unaware, application programming interfaces, popularly known as APIs, are highly crucial for creating a bridge between an input and realtime update on the same.

In the context of API integration in legacy banks, an API can help a financial institution to access modern cross-border payment networks, without having to completely upgrade the system or replace it with the latest tech and software.

APIs are high-performance solutions that can easily offer the latest exchange rates, status of transactions, and more to legacy banking systems, making them a perfect choice for quickly adopting cross-border transactions.

Several API providers and platforms offer this integration, Convera, Stripe, J.P Morgan, Wise, etc., to name a few.

Keep in mind that these 4 technologies are already implemented in several cross-border solutions, which also offer a proof of concept and can justify the investment directly.

The mentioned technologies and cross-border payment trends are just the tip of the iceberg. With more and more advancements in AI applications in fintech industry, it is only going to go above and beyond from here.

Conclusion

The technological innovations do not stop here, as businesses today can easily automate the entire process, from releasing funds to accepting payments and settling the ledger. The idea of using tech to improve user experience has always been the ultimate driving force for innovations.

With that said, we have reached the end of this post. Hopefully, you now understand the core technological advancements that have been powering the growing use of cross-border payment systems.

Thanks for reading, good luck!